This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Gap insurance can be a smart option to consider when buying a car. This insurance helps pay off what you still owe if your car gets totaled, and the payout from the insurance doesn’t cover the full loan amount. You might not need it for shorter loans or if you’re making a large downpayment.

As the finance manager, he reportedly took cash downpayments and funneled them into three credit cards not registered in his name. They put fraudulent info on my insurance that wasn’t there consent they didn’t have the right person on the insurance or the paper work. star rating. Do not go to dealership.”

A man in Arizona says that his gap insurance denied his claim due to a 60-cent clerical error during the initial purchase. Standard car insurance, like collision and comprehensive coverage, will pay you the car’s current market value if it’s totaled in an accident or stolen. That’s where gap insurance comes in.

Proof of Insurance Before driving off the lot, youll need to show proof of insurance. If you dont already have a policy, our team at Car Cloud Auto Group can help you connect with local insurance providers in Stafford VA. DownPayment (if required) While not a document, having a downpayment ready can speed up the process.

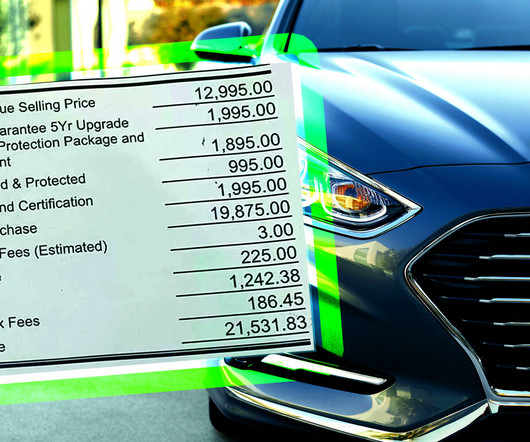

When purchasing a used vehicle, making a good downpayment is crucial not only for reducing your overall loan amount but also for securing favorable financing terms. The ideal downpayment can vary based on personal finances, the lender’s requirements, and other factors. 20% DownPayment: This totals $3,000.

If you’re considering whether to apply your downpayment toward covering negative equity or if you should use it for a newer vehicle, it’s essential to understand the implications of each choice. These losses can sometimes outpace the rate at which car owners pay down their loan balances.

Insurance considerations are equally important. Different car models and makes come with varying insurance premiums. Consider the insurance cost before making a final decision, as this will be a recurring expense. This involves understanding the impact of credit score and the various downpayment options available.

These are the insurance cost, fuels, repairs, taxes, and depreciation. Insurance Car insurance is mandatory by the law and forms a pretty significant portion of the overall ownership cost. The average premium that is paid for car insurance in Austin on a used car is in the range of $1,200–$1,500 annually. per gallon.

However, that low price comes with a catch: it requires a hefty downpayment (which we don’t recommend—more on that below), bringing the real monthly cost closer to $238. Prospective buyers should keep in mind that putting cash down on a lease is generally not advisable. Oh, and it’s only available in Denver.

For example, if there’s a £1,000 deposit contribution, that amount goes toward your downpayment, reducing what you need to put down yourself. With PCP, you pay lower monthly payments because a large portion of the car’s cost is deferred until the end of the agreement.

With no downpayment and minimal initial expenses, rental services provide the means of transport you need. Also, insurance coverage will be available as well relieving renters from all these concerns. Rental agreements typically include insurance coverage, registration, and other administrative tasks.

As a new car owner considering purchasing a 2025 Honda HR-V, you might be facing numerous questions regarding insurance options. One of the critical aspects of vehicle coverage is GAP insurance. GAP insurance, which stands for Guaranteed Asset Protection, plays a significant role in the event of a total loss of your vehicle.

If you’re still paying off a vehicle loan, there’s a chance that the insurance payout might not cover the full amount you owe. This is where Guaranteed Asset Protection (GAP) insurance comes into play, providing crucial financial coverage to bridge this gap. What Is GAP Insurance? Why Is GAP Insurance Important?

Consider making a larger downpayment, which can further enhance your negotiating power and reduce the borrowed amount. Refinancing can lead to reduced monthly payments and overall savings, providing financial flexibility for other priorities.

For example, used commercial vans are cheaper to insure and repair. And here’s the best part: the low price also translates to more affordable insurance and registration costs. This can raise your insurance rates, which can burn a hole in your pocket depending on how much you’ll have to pay the insurance company each month.

A good rule of thumb is to keep your total car-related costs (loan payment, insurance, fuel, and maintenance) around 10-15% of your monthly income. Questions to Ask Yourself: How much can you put down upfront? What’s a realistic monthly amount for car payments, insurance, and upkeep?

Consider all associated costs such as insurance, maintenance, and fuel. DownPayment: A substantial downpayment can lower your monthly payments and the overall interest paid over the loans term. A longer term may mean lower monthly payments but can result in higher overall interest costs.

Preparing for Future Purchases When preparing for future vehicle purchases, consider the following: Building Larger DownPayments: Aim to save for larger downpayments, which can mitigate the likelihood of negative equity. For more on insurance nuances, check out our insights on GAP insurance considerations.

With a $2,500 downpayment, I was only planning on financing $29,707. However, when I got the buyers order, the out the door number was $34,488.80, without GAP insurance. . “When submitting my application online, the out the door number was $32,207 with GAP.

Insurance Costs: Depending on the provider, insuring two cars can sometimes yield a discount as multiple policyholders may qualify for savings. Consider the following: Monthly Payments: Will the combined payments fit comfortably within your budget? Can you negotiate for lower monthly payments on both?

This blog post will delve into the essentials of lease agreements and gap insurance, offering insights on why they matter and how they can protect you financially during your leasing experience. Understanding Gap Coverage Gap coverage is an optional insurance policy that is particularly important for leased vehicles.

Insurance Claims: If you have insurance, contact your provider to report the accident right away. Assessing the Damage: If the vehicle is repairable, discuss options with your insurance agent. If the car is declared a total loss, your insurance will typically issue a payout based on the car’s current market value.

Basic Characteristics of the Lease Examine the lease terms, including length, monthly payment amount, downpayment, and interest rate (often called the money factor). Consider also the residual valuethe estimated value of the truck at the end of the lease, which can influence your monthly payments.

Save for a Big DownPayment Spreading out your term length can lower your monthly rate, but it often results in a higher total purchase cost due to accumulated interest. As much as possible, it’s best to pay a larger downpayment—one of at least 20% would suffice. The price tends to increase the longer you own the car.

When you start leasing a vehicle, you must make a downpayment. However, this downpayment is significantly lower compared to buying a car outright. No DownPayment, Manufacturer’s First Payment: Honda and Acura may pay the first month’s payment, so you can have a zero downpayment with only initial fees.

Some things you can do to boost your credit score include: Keep all accounts current Don’t open too many new credit accounts Have credit report errors fixed Make A Larger DownPayment Many financial experts suggest putting down at least 10 percent for a downpayment for a pre-owned vehicle.

DownPayment A larger downpayment reduces the amount you need to finance, which can lower monthly payments and potentially lead to better loan terms. Determine Your Budget Before starting the shopping process, calculate how much you can afford for a monthly payment.

F&I (Finance and Insurance) A department within a dealership responsible for arranging financing and insurance for customers purchasing vehicles. The F&I manager will also offer additional products such as extended warranties and GAP insurance. This is also known as being “underwater” on your loan.

Some households allocate up to 30% of their monthly budget to vehicle-related expenses, including payments, insurance, fuel, and maintenance. One promising approach is to focus on reducing monthly payments, which are crucial for many consumers. Leasing has re-emerged as a key strategy to achieve this goal.

Budget: What is your budget for both the purchase price and ongoing expenses like insurance and fuel? Gather financing offers from each dealer and consider: Interest rates Loan terms Downpayment requirements Incentives and Rebates Inquire about any manufacturer incentives that may be available at each dealership.

Lease-purchase Plan: This type of lease favors trucking entrepreneurs with bad credit or who lack the funds for a downpayment. However, this leasing arrangement carries a high-interest payment. When the lease expires, you can purchase the truck for its residue value or allow the leasing company to sell it.

Financing and Your Budget Whether you repair or buy, think about your budget : Upfront costs : Buying a used car might mean a downpayment and possibly a loan. Make sure you factor in monthly payments, interest rates, and insurance. Will more repairs pop up soon?

They may encounter terms and concepts like APR (Annual Percentage Rate), credit scores, downpayments, and loan terms, which can be confusing. Consider these strategies: Transparent Pricing Models: Clearly outline all costs associated with financing, including interest rates, documentation fees, and insurance.

Consider these costs: Deposit : Many financing plans will require a downpayment upfront. Monthly payments : Choose a plan that fits comfortably within your monthly budget. Additional costs : Don’t forget about insurance, maintenance, fuel, and road tax.

Being upside down on a car loan simply means that you owe more money on the loan than the car itself is worth. This can happen for a few different reasons, such as if you financed the car for a longer term or if you made a small downpayment.

Stability in Payments: After the loan is paid off, you are left with no more monthly payments, which can enhance your financial freedom. Depreciation Risk: New cars depreciate quickly, and you may lose value much faster than you can pay down the loan. Determine what aligns best with your needs and budget and proceed accordingly.

They also can cost less to insure and allow buyers to enjoy more of the features they love. You’ll need to consider the downpayment, the value of your trade-in , and the monthly payment. Many drivers have realized the advantages of buying used instead of new.

Be realistic and factor in costs beyond the car’s purchase price, such as insurance, maintenance, and fuel expenses. Understanding the terms of loans, interest rates, and payment plans can help you make an informed decision that suits your financial capabilities.

Your budget should clearly reflect what you can afford to spend, keeping in mind both the initial cost of the car and ongoing expenses like fuel, insurance, and maintenance. How much do you have left after paying for necessities like rent, food, utilities, and other regular payments or debt obligations?

Do you have enough savings to cover the downpayment or purchase price? Understand Ownership Costs: Factor in insurance, maintenance, and fuel costs associated with vehicle ownership as you prepare for this transition. Is the vehicle still suitable for your lifestyle, especially if your family or job situation has changed?

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content