This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Gapinsurance can be a smart option to consider when buying a car. This insurance helps pay off what you still owe if your car gets totaled, and the payout from the insurance doesn’t cover the full loan amount. You might not need it for shorter loans or if you’re making a large downpayment.

A man in Arizona says that his gapinsurance denied his claim due to a 60-cent clerical error during the initial purchase. That’s where gapinsurance comes in. Gapinsurance acts as a financial safety net. That’s where the gapinsurance was supposed to come in and cover the rest.

One of the critical aspects of vehicle coverage is GAPinsurance. GAPinsurance, which stands for Guaranteed Asset Protection, plays a significant role in the event of a total loss of your vehicle. What is GAPInsurance? Why Consider GAPInsurance When Buying a New Vehicle?

If you’re still paying off a vehicle loan, there’s a chance that the insurance payout might not cover the full amount you owe. This is where Guaranteed Asset Protection (GAP) insurance comes into play, providing crucial financial coverage to bridge this gap. What Is GAPInsurance?

If you’re considering whether to apply your downpayment toward covering negative equity or if you should use it for a newer vehicle, it’s essential to understand the implications of each choice. These losses can sometimes outpace the rate at which car owners pay down their loan balances.

For example, if there’s a £1,000 deposit contribution, that amount goes toward your downpayment, reducing what you need to put down yourself. With PCP, you pay lower monthly payments because a large portion of the car’s cost is deferred until the end of the agreement.

However, that low price comes with a catch: it requires a hefty downpayment (which we don’t recommend—more on that below), bringing the real monthly cost closer to $238. Prospective buyers should keep in mind that putting cash down on a lease is generally not advisable. Oh, and it’s only available in Denver.

Understanding the interplay between leasing and gap coverage is crucial to preventing potential financial setbacks in the unfortunate event of a total loss. This is where gapinsurance comes into play. It covers the difference, or gap, between what you owe on your lease and what the insurance payout is.

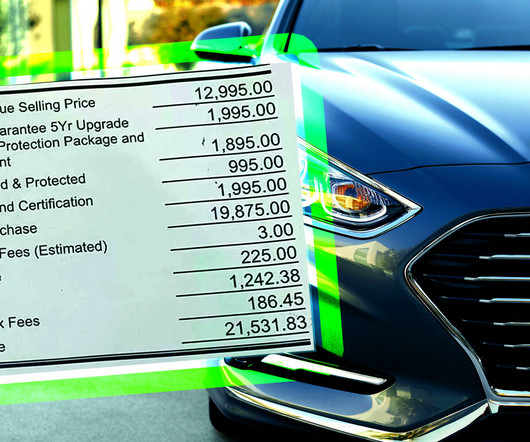

. “When submitting my application online, the out the door number was $32,207 with GAP. With a $2,500 downpayment, I was only planning on financing $29,707. However, when I got the buyers order, the out the door number was $34,488.80, without GAPinsurance.

Preparing for Future Purchases When preparing for future vehicle purchases, consider the following: Building Larger DownPayments: Aim to save for larger downpayments, which can mitigate the likelihood of negative equity. For more on insurance nuances, check out our insights on GAPinsurance considerations.

F&I (Finance and Insurance) A department within a dealership responsible for arranging financing and insurance for customers purchasing vehicles. The F&I manager will also offer additional products such as extended warranties and GAPinsurance. It’s often used as a starting point for negotiations.

Stability in Payments: After the loan is paid off, you are left with no more monthly payments, which can enhance your financial freedom. Depreciation Risk: New cars depreciate quickly, and you may lose value much faster than you can pay down the loan. Determine what aligns best with your needs and budget and proceed accordingly.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content